DAO-ing without going to jail

A proposed structure by Andreessen Horowitz

I’ve followed developments in DAO-world through headlines and tweetstorms, but as I don’t operate a DAO treasury, the legal/tax issues related to operating one have been opaque to me.

In October, a16z published a proposed legal framework for DAOs, attempting to illuminate a path that is currently shadowy and fraught with FUD. It’s an extensive 30-page piece written by a legal consultant and a16z’s General Counsel in what I consider hard-to-read legalese (sorry. Maybe i’m just dense.)

This is my layman, business person interpretation of the ideas in the paper.

80% of the content is straight from the paper, 20% is personal knowledge/reactions. I’m writing it to make sense of the ideas in there, and to share with others who may not be inclined to trudge through 30 pages of legal speak. Tweet/Share if you find it helpful.

Context

DAOs were initially founded to substantially decentralize operations, compel community participation, and experiment with autonomous organizations through the deployment of smart contracts (e.g. MakerDAO).

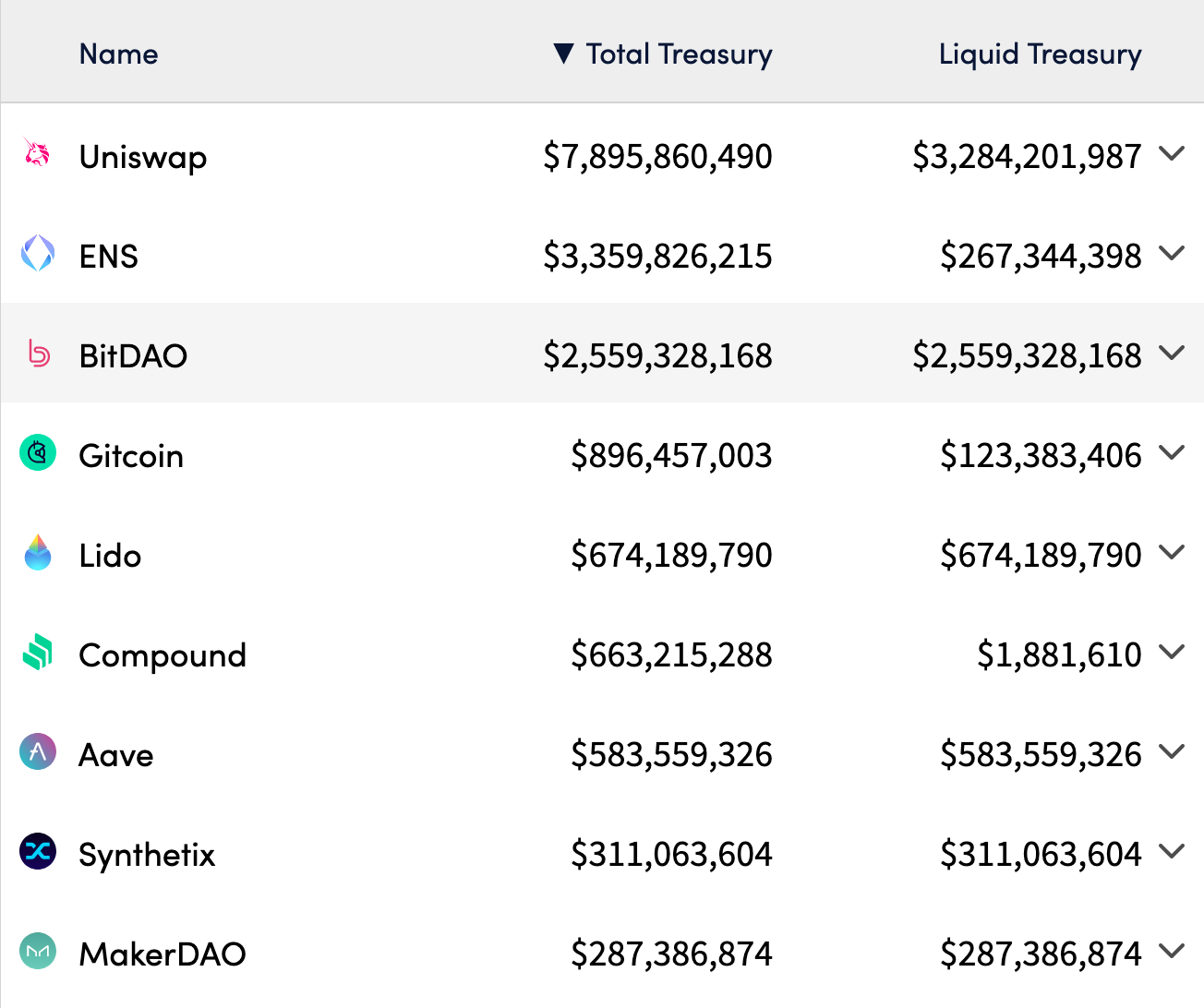

In the last few years, many DAOs were created to manage massive treasuries generated by the creation of successful networks. e.g. Uniswap, ENS, both protocols with multi-billion dollar treasuries.

Other than DAOs created in conjunction with protocol launches, DAOs have also been created by self-starting groups of individuals with a specific angle (e.g. crypto builders, NFT enthusiasts). They actively look for ways to deploy assets contributed by their members (super high level overview).

If you’re like me, you might ask, why do we need a DAO to decide on how to spend funds? Wouldn’t a small, centralized group of delegates working actively on these projects be more efficient at deciding how the money is spent?

Perhaps it would be more “efficient,” but in today’s crypto environment, where the value of a network, quantified by activity volume and token price, lives and dies on participation from the community. Participation feels like having the power to make impactful decisions, which creates a virtuous cycle of involvement - the more impact I can make, the more I participate, the more impact I can make…

Sounds great, not just for users but also project creators/managers! Some of them presume an abdication of centralized decision making absolves them of obligations and liabilities related to managing a big pot of “money” (or utility tokens, or securities, whichever the case may be).

Now, regulators like the IRS and SEC in the U.S. are catching up, and people are worried about being caught unawares. People are tuning into the risks of DAO management.

Just voting on a website like Snapshot.org could expose DAO members to liabilities arising from harm sustained from DAO activities, and to tax liabilities. Multisig key holders are especially at risk given their direct relationship to actions taken by the DAO.

Mark Lurie described it well in a recent article in The Defiant:

Remember, the original purpose of a corporation was to limit personal liability. Before corporate entities, everybody had unlimited liability for anything that happened to one of their ventures. If an investor owned a ship that smashed into a dock, for instance, the dock owner could sue the shipping company and its owners for damages… DAOs without a corporate entity expose all their members to unlimited liability, turning back the clock on centuries of risk management.

In addition to punitive ramifications, practical difficulties exist in the running of DAOs - how do you get a bank account (who’s the account owner), who signs contracts with third parties (who holds third parties accountable / who can third parties hold accountable)?

The paper proposes a solution to the above problems related to DAO management.

What we want out of a DAO structure

Things to achieve

Create a taxpayer capable of paying taxes within the US, especially for transactions undertaken by the DAO treasury

Be able to open a bank account

Be able to sign legal agreements with third parties

Facilitate decentralization by constraining the decision making power of any one individual/entity

(My addition:) An easy way to update the membership of the DAO (add, remove)

Things to protect from

Limit the liability of developers and members. Most DAO members are unaware of the liabilities they face under today’s DAO structures, which look like partnerships whose liability is not limited. These liabilities could be faced as a group, or by each individual

Keep governance token holders from being individually responsible for tax/financial reporting obligations arising from DAO treasury management

Minimize the risk of imputing ownership of DAO treasury tokens to governance token holders

The first 8 pages are basically dedicated to scaring people into acknowledging the far-reaching and increasingly broad tax reporting obligations related to crypto (rightfully so), including a reference to the Infrastructure Bill. It looks like there are more words in the footnotes, referencing IRS announcements and related analyses, than in the main body of the paper; this is a reflection of how onerous and convoluted the situation is today, sadly. It’s not clear if the IRS has the resources and motivation to police all of these violations, but I suspect nobody wants to play roulette with their freedom.

Taxable DAO events

These three DAO treasury activities could constitute events that require tax reporting and payment:

Staking and liquidity mining programs, which can look like income generation or capital gains

Treasury diversification, where the DAO exchanges its own native tokens for other tokens in an attempt to weather volatility in the value of its own token. This obviously counts as liquidation of an asset that would require in tax reporting

No matter how many times I re-read the paragraph, I still couldn’t understand a point they tried to make about Grant/lobbying grants being subject to tax (a grantor gets taxed on grants, like you have to pay taxes on giving away money? Sounds wild to me. Or do they mean these grants are not tax-deductible for tax computation?). Oh well, I leave you a direct quote: “Grant/lobbying Programs… a disposition of a treasury’s governance tokens… would be taxable…”

Common structures adopted today

Currently, there are the two legal structures (or lack thereof) adopted by most DAOs:

(A) No formal structure/no entity

Some have chosen this path in an attempt to avoid extensive administration burden. Sure, the anarchy types prefer to opt out of “the system” entirely. But for those actually willing to formalize their structure, today’s commonly available structures would aggregate power into the (reluctant) hands of their official Directors/key persons, negating the core raison d’etre of the DAO.

Some DAOs also haven’t yet defined an explicit business purpose, which disqualifies them from the usual entity types (and some may never define one, as they are expressly focused on spreading the adoption of technology rather than the pursuit of profit).

Unfortunately, opting out of creating a legal entity does not mean you can opt out of the legal system. From a legal perspective, two or more individuals engaged in even a tenuous business relationship could constitute a general partnership.

Wyoming’s DAO law is a good first step for society to recognize the legitimacy of DAOs, but until such a concept is recognized federally, it doesn’t offer sufficient protection from open questions with the SEC or IRS.

This is the opinion held by the paper’s authors, and a commonly shared one, but I don’t fully understand. I’d love it if someone else can provide a concrete example of where and how DAOs can thread a needle through this state of affairs - and where they simply cannot. Perhaps we could take inspiration from the evolution of cannabis regulation, where state and federal laws have clashed. (Fun digression: 2-page FAQ on how to register a Wyoming DAO.)

(B) Offshore entities

DAOs have been incorporated by US persons/projects in places like the Cayman Islands, BVI, Panama, Singapore, Ireland and Switzerland. This is favorable from an operational flexibility perspective, and a tax perspective.

But the IRS, and US law enforcement in general, has extremely long arms.

If financial value was created by US persons/business, you can expect the IRS to want a piece of the action. If US persons/businesses were harmed, and it behooves the administration’s crypto strategy to move on a complaint, I would be shocked if they didn’t succeed in enforcing. If there were a better alternative, offshore structures may result in more legal grey area/risk than is worth it for DAO projects.

Proposed structure: the UNA

Some DAOs are structured to make profits for its members. For example, Metacartel Ventures (https://metacartel.xyz/) is a venture DAO composed of crypto builders and influencers that invests in early stage dapp with a profit motive. PleasrDAO (https://pleasr.org/) is a group of artists and influencers that collects NFTs expecting an appreciation in value.

However, this paper focuses on DAOs that are structured in order to manage treasuries, which in most cases do not have profit-making as a core objective.

In this case, the proposed structure is an “UNA,” which is a type of organization endorsed in the US as early as 1996. It sounds hip enough to conjure mental images of rainbows and unicorns, but it’s actually a stodgy acronym of “Unincorporated Nonprofit Association” (sorry).

A DAO would have its members enter into an agreement to become an UNA, which would give it legal form to open a bank account, sign contracts, and pay taxes - and most importantly, provide more liability protections for its members than under the “no structure” route.

What’s “unincorporated” about an UNA? Incorporated entities (“Inc.”), aka “corporations,” are legal entities created to pursue a business venture; they are often more onerous and costly to maintain, and, significantly, you will need an explicit for-profit business purpose - many DAOs will fail this test. Unincorporated associations don’t require the explicit creation/registration of such an entity; as long as a few people get together to do something, they can be considered an unincorporated association (e.g. a church, general partnerships); members still could be subject to personal liability if something goes south and the separateness of the association from the individuals isn’t respected, but this is much less likely than if there were no entity at all.

What is “nonprofit” about an UNA? Many DAOs and DAO treasuries are formed to foster the growth of their ecosystem. They are not created explicitly to create profits for the members of the DAO. Therefore, DAOs often classify better as a nonprofit rather than a for-profit.

The authors propose two specific approaches in registering the UNA:

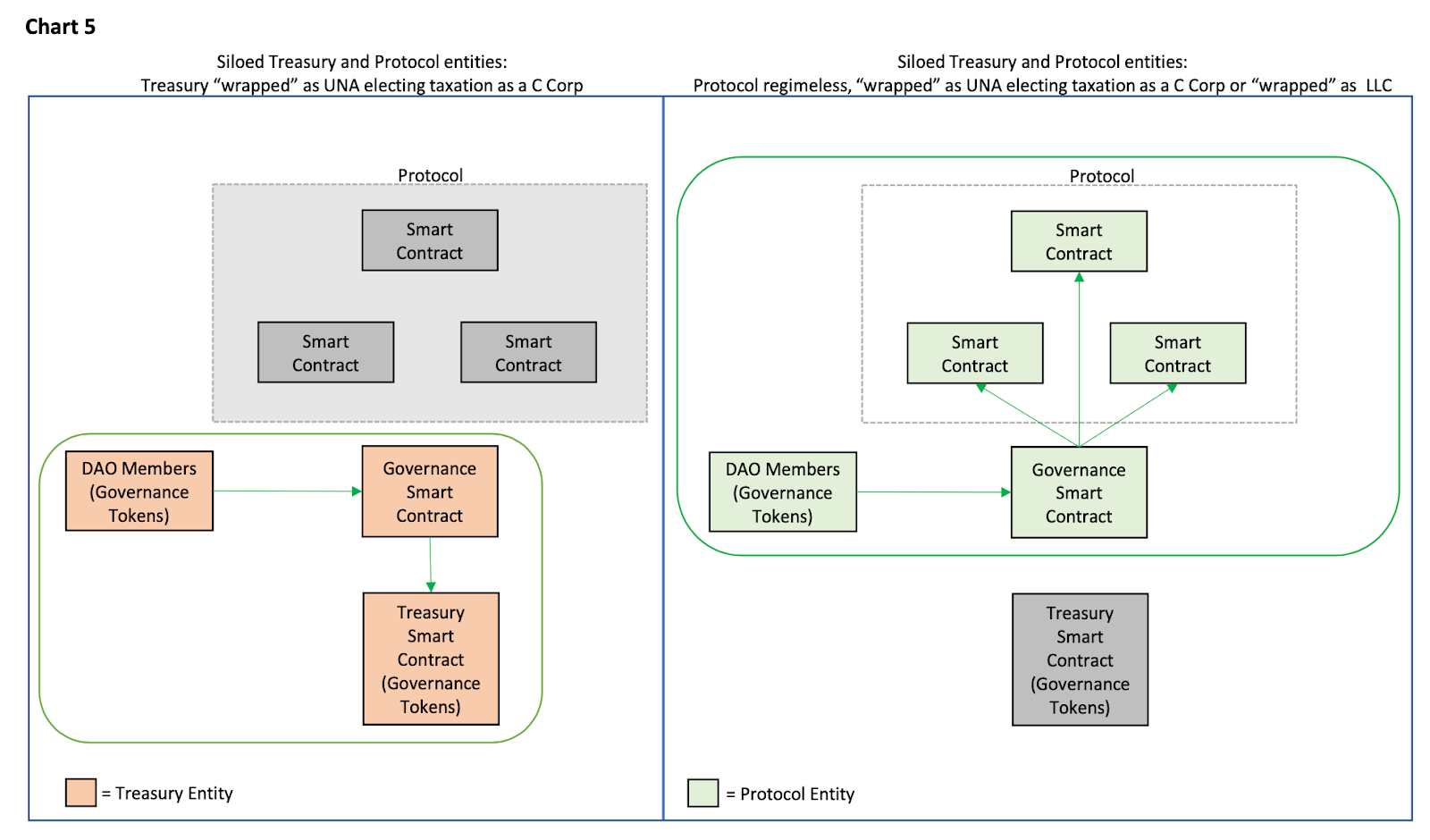

Wrap everything in an UNA (the protocol + the treasury)

In the first approach, the UNA includes both the protocol and the DAO treasury. This provides maximum liability protection, but risks constraining what the DAO can or cannot do in the future.

Wrap the treasury in an UNA, keep the protocol separate (“Siloed” approach)

In the second approach, what they call the “Siloed” approach, the UNA could cover just the DAO treasury, since it’s the treasury that will engage in the majority of taxable transactions.

The protocol itself could abstain from forming an entity until later, or choose to register itself as a separate UNA or an LLC.

This would allow the DAO to undertake activities separately from the treasury (e.g. the DAO could later decide to pursue for-profit activities, without jeopardizing the nonprofit status of the treasury UNA).

Approach 2 feels like the best option, given how fast things change in crypto. If your strategic, more impactful protocol decisions are hampered by restrictions on the treasury UNA-DAO, at some point the community is likely to get frustrated.

Tax reserves

There is a final idea I found particularly interesting: have a reserve created for tax payment on each taxable transaction. For example:

When the treasury participates in yield farming and generates income, the smart contract will auto-magically deposit some percentage of the income into a wallet owned by the treasury. The treasury can then immediately liquidate the tokens into stablecoins (and eventually into US dollars), which will be held to make tax payments.

This saves the DAO treasury operators from worrying about passing a vote each time to make IRS payments (can’t imagine how much fun that would be with the kinds of people we have in crypto), and saves them from the risk of not having enough USD value to make the tax payments in an environment of price volatility.

Reflections

While most DAO members are giddy with enthusiasm for the newfound power of decentralized governance, many are gradually wising up to the risks entailed. I’m part of virtual city DAO which pulled back their treasury management launch due to risks uncovered at the last minute.

At the same time, I don’t think the UNA is the last word on optimal DAO structures. It still feels too amorphous to me, and is incompatible with an increasingly important feature of DAOs, which is to generate income/profits for its members. Other forms and structures will be proposed, solving different problems for different DAO designs.

The frenetic pace of development of DAOs, and the innovations they keep churning out, makes it feel like DeFi all over again. In the same vein, I suspect the regulators aren’t going to keep up.

When regulators do catch up, enforcement won’t be applied uniformly (nor fairly) against all players. As an example of uneven enforcement, look at Celsius and BlockFi being singled out by federal and state regulators.

If I helped manage a DAO, I’d dedicate a good chunk of my time towards (a) strategizing how to stay nimble in the face of uncertain regulation, and (b) balancing the expectations of members against reality; mob members sometimes make it impossible to take reasonable courses of action.

Thanks to Brandon Ferrick, GC of the DeFi R&D company Injective Labs and Nicolas Arqueros, CEO of EVM-builder dcSpark, for input and feedback on this article.

Click here for a PDF version of this article.

Thank you for this article. Do you know what are the advantages to set tup a foundation in BVI or equivalent countries?